Personal Finance

•

6 mins read

•

October 27, 2020

The Basics of Buying Rental Property Explained

Demystifying the owning and operating of rental properties

Few people pile up enough wealth to retire overnight. You can invest in the stock market, and with patience and a bit of stock savvy, you might do very well–or you could lose your shirt. Another way to retire early that is a bit less risky is by investing in rental properties — be it a single-family home, a condo, townhouse, or an apartment complex.

The best thing about owning rental properties is that they provide long-term cash flow that allows you to potentially

that lasts for as long as you own the rental property. Like with anything, there are advantages and drawbacks. But if you want to retire early by purchasing and investing in real estate, there are a

.

What Is Rental Property?

Rental property are homes, condos, and apartments that are occupied by tenants who usually sign a lease or rental agreement for a specific time.

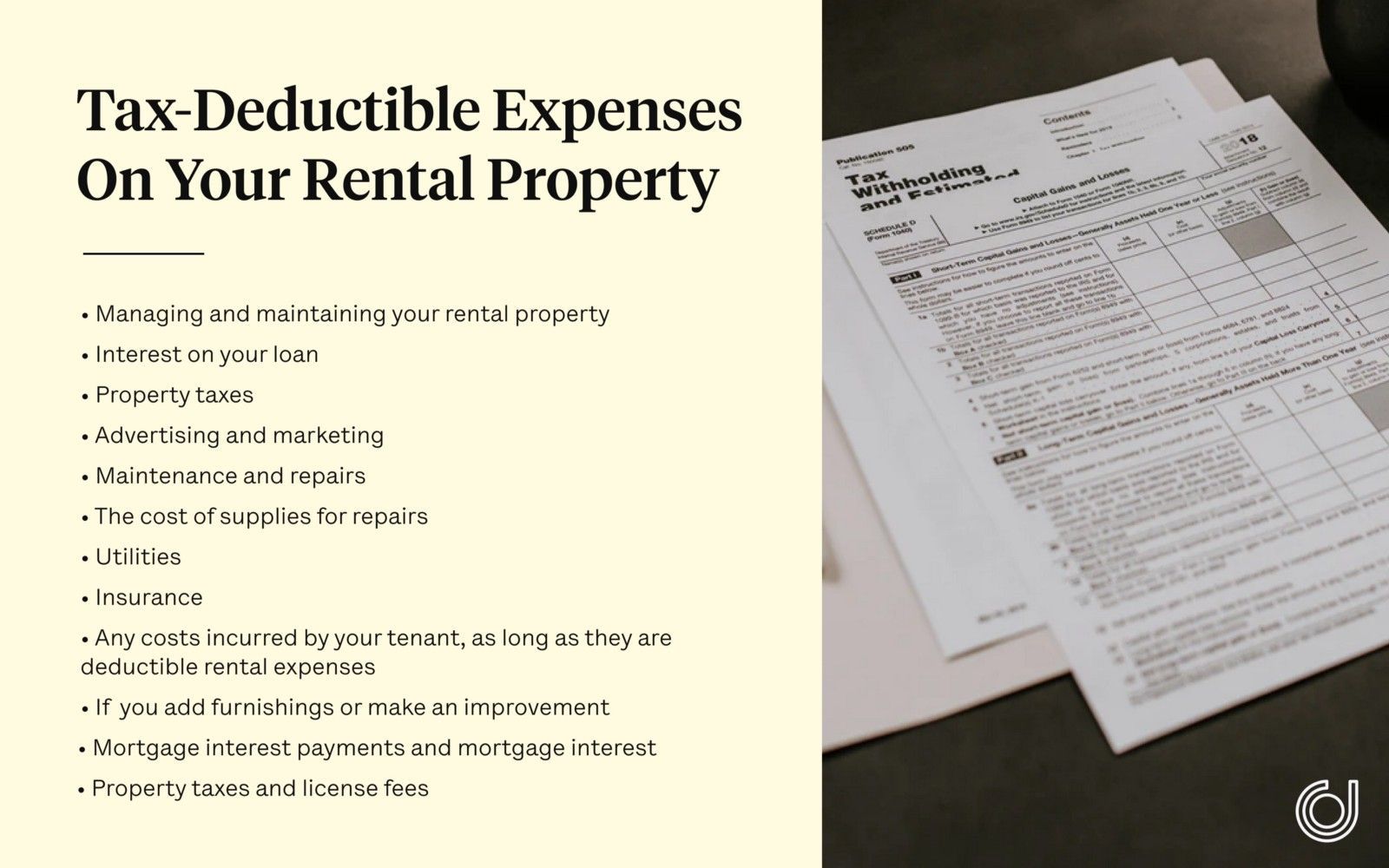

The Internal Revenue Service (IRS) defines rental property two ways. Vacation homes and permanent rentals. You are expected to report any rental property you own on your yearly tax return, but there are a dozen tax deductions that come with owning rental property that can reduce the overall cost.

The Basics of Buying Rental Property

First, you’ll want to determine the fair market value of the property, which is the value of the property on the date you make the purchase. Like buying any house, you don’t want to pay more than its worth. If instead the property was once purchased for personal use and made into a rental property, then the fair market value is based on the date it was converted.

Get in touch with a real estate agent that knows the neighborhood and see what properties sell for. You’ll also want to figure out how much you need in rent income each month. Say for instance, the property you want to buy will easily bring in $1200 each month in rent. Over a year, that’s $14,400. So the property offers a gross income of just over 14% on the purchase price. Figure in maintenance and updates to the property along with your mortgage payment, and your income will be less. But, it gives you a good idea what to expect.

Yes, there is. Of course, it also depends on where in the country you live in. If you live in the north where snowfall is common, then late fall or early winter is a good time to buy rental property. Around the holidays–Thanksgiving and Christmas, especially–are considered the best times, and if possible, on the exact day. Even in warmer climates, the same holds true.

That’s because there is less competition from prospective buyers. No one wants to move or sell a house on Christmas day. People also prefer touring homes when the weather is nice. In the summer, the competition goes up along with the sales price.

If possible, it’s also a good idea to track how long a particular property has sat on the market. The longer it sits, the more willing sellers become to push for a sale, which can often bring down the price.

Another consideration is how well a house, condo, or apartment complex shows. Heavy snowfall can hide wear and tear, like chipping paint or dead landscaping on the outside of the building. This also gives you time to make the interior as nice as possible so it rents fast come spring.

What Can I Leverage to Buy a Rental Property?

Most banks and credit unions typically require a 20% down payment when buying a rental property. That ensures you won’t be required to take out mortgage insurance and also makes you less of a risk to lenders.

But that 20% can mean a downpayment of thousands of dollars. That said, you can buy a rental property with no money down of your own. Some people use other people’s money, or get creative with financing. After all, the less you have to put down, the higher the return over time.

A couple of other ways you can leverage financing to buy rental property include:

1. Make the rental your primary residence (at least for a time).

2. Make use of seller financing–buy the home or condo from the seller rather than through traditional financing.

3. Leverage other property by using the equity you have built up in one property for a cash-out refinance.

5. Work out a deal with the seller to buy his or her mortgage outright.

6. Get a loan. A personal loan can be used for almost anything. That includes a downpayment on your rental investment.

7. Find a purchasing partner willing to help with the down payment.

Tax Advantages of Buying Rental Property

For real expenses related to your rental property, the IRS allows you to take a tax deduction, like for a mortgage interest payment, depreciation, or property taxes. However, you must record each expense, as per

. Why do they allow this? The real estate and mortgage industry together form an important backbone for the American economy and so the goverment frequently incentivises citizens to partake in home ownership.

What Are the Downsides to Purchasing Rental Property?

Although there are more than enough positives to buying rental property as a slow and steady way to retirement, there are also a few drawbacks. For one, if the housing market drops, so does the value of your rental property. You may still get the same rent from your tenant, but your property just won’t be worth as much until the market recovers.

Also, insurance and taxes on your rental property only go up. Your mortgage rate and term may be fixed, but unless you increase rent on your property, you may lose valuable cash flow. Then there’s the problem with tenants, or times when you have no one living there. Tenants may pay late, scatter litter or garbage around the property, irritating your neighbors, or they can be overly demanding.

While you can pick and choose your tenants (to a degree), you can’t control if the neighborhood and if house values decline. You can keep your property drop-dead gorgeous, but if properties around you fall into disrepair, your property value will fall also.

Then there’s the upkeep, maintenance, repairs, and modifications to the property that will fall on you as the rental owner and landlord. You can hire someone to take care of a leaky faucet, but you’ll fit the bill.

Buy Rental Property and Retire Early

It takes careful planning to buy rental property and make enough money to retire early. You will want to educate yourself about the complex nature of tax laws, contracts, tenants, write-offs, regulations, and more. You must also know what you’re getting yourself into before you jump in. But rental properties–done right–can provide long-term cash flow that will allow you to potentially generate a strong stream of passive income.