Personal Finance

•

9 mins read

•

April 22, 2021

How Often Does Your Credit Score Update?

Read on to learn how long TransUnion, Equifax, and Experian take to update that all-important credit score.

If you’ve ever been snubbed for a loan or credit card, you know how important your credit score can be. And, if you’ve put a lot of energy into improving your credit score, you also know that

. Upgrading your score can take time. In fact, it can seem like it drags on forever.

But just how long do you have to wait for your credit score to update?. What is a Credit Score?

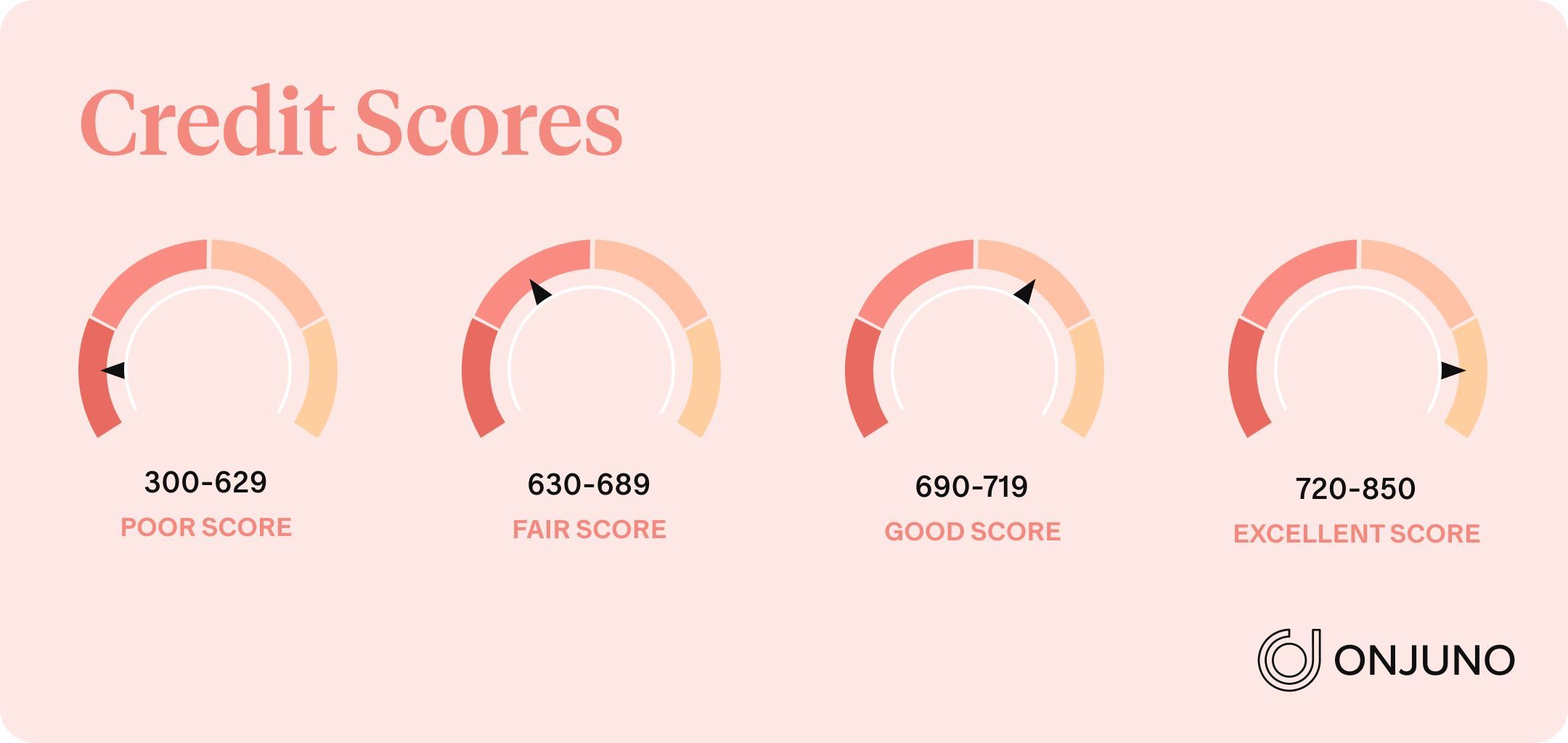

A credit score is a three-digit number that ranges from 300 to 850. The number reflects how well you pay your bills on time.

A good to excellent credit score is essential

, a house or when you sign up for a credit card. Your score can even make a difference when renting an apartment or qualifying for the best interest rates.

How Often Does Your Credit Score Update?

When you think of credit score ratings, it’s a sure bet the three big credit agencies come to mind: TransUnion, Equifax, and Experian. Each of these bureaus can update your credit instantly, monthly, or whenever lenders provide new information.

All it takes is a positive or negative change to your information. It’s also possible that differences in your score result from which credit score system — FICO or VantageScore — is used to calculate your score.

What is FICO?

The Fair Isaac Corporation or

is a method of evaluating and calculating your creditworthiness. Credit scores range from 300 to 850.

Every once in a while, FICO updates its methodology. The new

is the most recent version, announced in January 2020.

What is VantageScore?

Like FICO, VantageScore also evaluates your creditworthiness. The most recent update to

incorporates machine learning to give lenders more confidence when extending terms.

So, how long does it take for each of “the big three” to move the needle up or down on your credit score?

TransUnion

TransUnion updates your credit report

. You may not see an immediate change, but instead, a line that reads, “date updated.” This is the most recent day information given to TransUnion by a lender.

But not all lenders provide information in the same way or at the same time, so updates may not appear right away.

TransUnion makes a point to say that your credit score

. That’s nice to know, especially if you’re planning a big purchase in the next few days.

Even so, rapid rescoring with TransUnion can be

to your credit score, but they haven’t yet shown up on your report.

Here's how it works:

* If you’ve made positive credit moves in the last couple of days, but you don’t see them on your reports, you can ask a lender to request the information be added.

* The lender must make the request on your behalf, and you’ll likely be charged a fee.

* Keep in mind that you can’t make a rapid rescore request on your own, and it won’t fix any past mistakes or make any negative information on your report disappear.

Equifax

Much like TransUnion,

recalculates and updates your credit score about two to three days after a creditor sends over an active inquiry. Depending on their reporting cycle, creditors will report to the three credit bureaus about every 30 to 45 days.

Unfortunately, that means that a company checking your credit score with Equifax might get an out-of-date credit score for you, simply because reports are only made every month or month and a half by creditors.

Plus, if Equifax feels something looks a bit fishy, it will verify the information before it goes into your report. This might take a few hours or a few days, but it can delay your report from being updated quickly.

Experian

Not all creditors or lenders report to all three credit reporting agencies. A lender might send a report to TransUnion this week, but not get it to Experian until next week (or vice-versa). That makes pinning down an exact date when Experian updates your credit score difficult.

With

, it is possible for your credit score to change daily or weekly. This depends a great deal on how many active credit accounts you have. It also depends on the time of day your report happens to get updated.

Under Biden’s plan, the

. Instead, a public registry would be housed under the Consumer Financial Protection Bureau (CFPB). A paper was presented by the Dems in 2019 and is set to be approved or rejected this year or early 2022.

When Do Creditors Report to Credit Bureaus?

Most creditors send information like a large purchase, opening a new credit card, applying for a mortgage, making a late payment, etc., to the bureaus once a month.

But not all creditors report to all bureaus, and they might report at different times during the day. Some credit card companies that handle millions of accounts may only send over information in batches, once or twice a month.

That’s one reason why moving the needle from “poor” to “excellent” credit won’t happen overnight. Your score can move a bit in one day, but it can take a while to make a real change for the better.

How Often Should You Check Your Credit Score?

The simple answer is that you can check your credit score whenever you want. And, your credit score won’t take a hit just because you can’t stand not knowing.

Besides, there are times when checking your score more often is a good idea:

* If you’re worried your credit information has been compromised

* To protect yourself from identity theft

* When opening a new credit card

* When applying for a mortgage or a personal loan

* When you’ve been working on improving your credit score

For most people, checking credit scores annually is adequate. That’s not to say that checking your credit score more often, say every three months, is not also a solid plan. Doing so will actually give you a better idea of what goes into raising or lowering your score and credit history over time.

While day-to-day progress is informative, it will only give you half the picture — whereas checking less often helps you identify trends and is a better indicator of your credit history.

How to Check Your Credit Score for Free

At one time, you’d pay a fee to check your credit score. But over the years, dozens of resources have popped up, including most banks and credit unions, where

.

The type of score you get will vary a bit, depending on if it’s your FICO score or from VantageScore. The easiest way to check your credit score is most likely from your credit card company.

Give Credit Where Credit is Due

Although credit scores are updated daily, sometimes twice a day, it doesn’t mean that your score will take the kind of upward jump you’d like to see happen quickly. It takes time to raise a score of 630 to 850. And, it’s easier to see your score go the other direction — straight down.

Pay your bills on time, don’t open

, or apply for credit over and over again, and you can go from zero to hero all in good time!